As a taxpayer, you’ve undoubtedly heard about adjusted gross income, or AGI, which plays a pivotal role in your taxes. Let’s take a deep dive into what AGI is and why it’s so important.

Note: The One Big Beautiful Bill (OBBB) is now also being referred to by lawmakers as the Working Families Tax Cut Act. You may see one or both names used here, but they refer to the same set of tax changes.

At a glance:

- AGI is your gross income minus specific adjustments, which the IRS uses to determine your taxable income.

- Calculate your AGI by subtracting adjustments from your gross income.

- Your AGI can determine your eligibility for certain tax breaks.

What is adjusted gross income (AGI)?

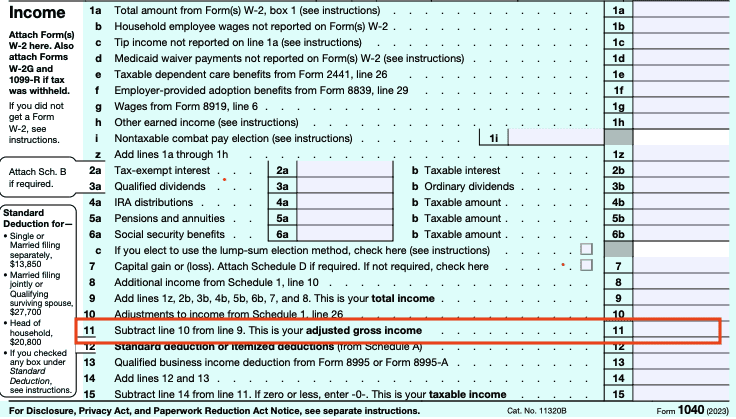

Essentially, your AGI is your gross income minus any adjustments. The Internal Revenue Service (IRS) uses your AGI to determine how much tax you owe, and it can influence which tax deductions and credits you can take. It’s noted on line 11 of IRS Form 1040:

Understanding gross income

To understand AGI, we first need to define gross income. Gross income is the total income you earn in a year before any taxes or other deductions are taken out.

Common types of gross income

- Wages and salaries: Earnings from your job, plus any bonuses or tips.

- Interest and dividends: Money earned from investments like savings accounts, bonds, and stocks.

- Capital gains: Profits from selling capital assets like stocks, bonds, or real estate.

- Business income: Self-employment income or profits from running a business. This includes revenue minus any business expenses.

- Rental property income: Earnings from renting out property. This includes the total rent collected minus any deductible expenses like repairs and maintenance.

- Unemployment benefits: Payments received as unemployment compensation.

- Social Security: Any Social Security distributions you received.

Other types of gross income

- Alimony received: Payments received from a former spouse (only for divorces finalized before 2019).

- Royalties: Income from intellectual property such as patents, trademarks, or books.

- Gambling winnings: Any money you win from gambling activities, including lotteries, casinos, and betting pools.

Adjustments to income

You must make certain adjustments to your gross annual income to calculate your AGI. Makes sense, right? These adjustments are specific expenses that the IRS allows you to subtract from your gross income. They are also sometimes called above-the-line deductions — “the line” refers to your calculated AGI on your federal income tax return (Form 1040).

The deductions you can make depend on your personal tax situation. We will highlight some common income adjustments below, but don’t worry too much about them. If you use TaxAct®’s DIY tax preparation software, we will ask you detailed questions to determine what specific deductions you qualify for and guide you through the tax filing process.

Common adjustments to income (as of tax year 2025)

- Educator expenses: Teachers can deduct up to $300 of out-of-pocket costs for classroom supplies like books and equipment.

- Student loan interest: Eligible students may deduct up to $2,500 of interest paid on student loans.

- IRA contributions: Contributions to a traditional IRA may be deductible depending on your income.

- Health savings account (HSA) contributions: If you have a high-deductible health plan, contributions to an HSA are deductible.

- No tax on tips deduction: This new tax break lets you deduct qualified tip income. This deduction was introduced by the Working Families Tax Cut Act.

- No tax on overtime deduction: Also part of the Working Families Tax Cuts, this tax benefit lets you deduct qualified overtime compensation.

- Car loan interest: Another new tax break for interest paid on a qualified passenger vehicle loan.

Other adjustments to income

- Self-employment tax: Self-employed individuals can deduct half of their self-employment tax.

- Self-employed health insurance: If you’re self-employed, you can deduct the cost of your health insurance premiums.

- Moving expenses for military: Active-duty Armed Forces members can deduct military moving expenses if the move is due to a military order.

- Penalty on early withdrawal of savings: If you withdrew money early from a CD or another time-deposit savings account, you might be able to deduct the penalty.

- Certain business expenses: Some professionals can deduct specific work-related expenses.

- Contributions to SEP, SIMPLE, and qualified plans: Self-employed individuals can deduct contributions to certain retirement accounts.

- Alimony paid: For divorces finalized before 2019, alimony payments are deductible.

How to calculate adjusted gross income explained

Calculating your AGI is straightforward if you follow these steps:

- Start with your gross income: This includes all your earnings from wages, investments, and other sources discussed above.

- Subtract adjustments to income: Deduct the allowed adjustments such as educator expenses, student loan interest, and HSA or IRA contributions.

Need help? Try out TaxAct’s easy-to-use AGI calculator.

Example AGI calculation

Let’s review a more detailed example to illustrate how to calculate AGI with multiple types of income and adjustments.

Imagine your total gross income for the year as a single taxpayer includes:

- Wages: $50,000

- Rental income: $10,000

- Dividends: $2,000

- Business income: $8,000

- Gambling winnings: $500

Adding all those together, your total gross income would be $70,500.

Next, let’s say you had the following adjustments:

- Student loan interest: $2,000

- IRA contributions: $3,000

- Health savings account contributions: $1,000

- Self-employment tax deduction: $565 (half of $1,130)

- Self-employed health insurance: $2,500

Adding those together, your total adjustments would be $9,065.

Finally, subtract your adjustments from your gross income to find your AGI: $70,500 (gross income) – $9,065 (adjustments) = $61,435 AGI.

FAQs about AGI

The bottom line

Understanding your AGI is essential for tax planning purposes. By taking advantage of tax benefits and adjustments, you can potentially lower your taxable income and overall tax bill. And don’t forget, TaxAct can help you claim valuable tax deductions and simplify tax filing when you use our DIY tax prep software.

For more in-depth reading, you can visit the IRS website on AGI.

This article is for informational purposes only and not legal or financial advice.

All TaxAct offers, products and services are subject to applicable terms and conditions.