Updated for tax year 2025

Digital currency wallets like Coinbase® have made it easy to invest in blockchain technology, such as cryptocurrency. If you’re new to investing or crypto exchanges, you might be wondering how to report cryptocurrency on your taxes. On this page, we’ll walk you through the tax implications of selling crypto. We’ll also cover how to report gains and losses from digital assets when filing your income tax return.

At a glance:

- Selling crypto for a profit results in capital gains and needs to be reported on your tax return.

- Receiving crypto can also be a taxable event (e.g., receiving crypto as income or mining crypto yourself).

- Crypto donations are not subject to capital gains taxes and may earn you a tax deduction.

Reporting crypto on your taxes

Any time you make or lose money on investments you sold, including cryptocurrency held as a capital asset, you should report the transaction on Form 8949 and then summarize the result on Schedule D.

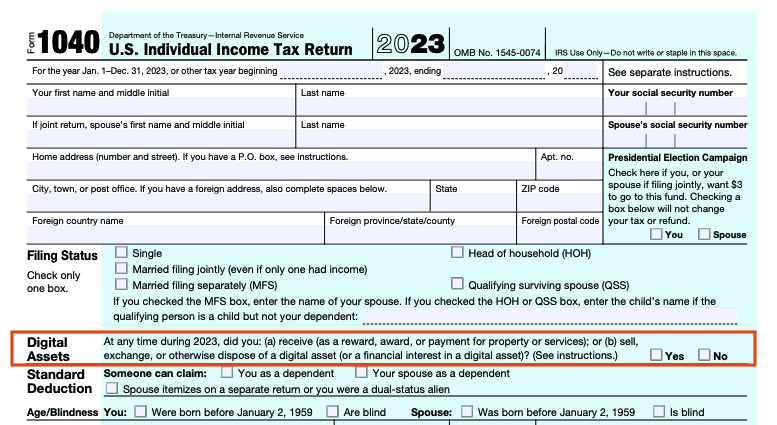

When filing Form 1040, U.S. Individual Income Tax Return, you’ll notice the IRS asks taxpayers about virtual currency for tax reporting purposes. The Digital Assets section is located under the section where you select your filing status.

On Form 1040, the IRS asks whether at any time during the year you received, sold, exchanged, or otherwise disposed of a digital asset or financial interest in one. You generally check “No” if your only activity was buying digital assets with U.S. dollars and/or holding them, or transferring them between wallets you own or control.

Note: If you used a broker to sell a digital asset, your broker may send you Form 1099-DA, but you still must answer the digital-asset question, regardless of whether you receive that form.

Taxes on crypto gains

When do I have to report cryptocurrency on taxes?

When you sell cryptocurrency as a capital asset, you incur a capital gain or capital loss that needs to be reported on your tax return.

- Short-term gains: If you profited from selling crypto you held for one year or less, it’s considered a short-term capital gain, and it would be taxed as ordinary income. Your federal tax rate would range from 10% to 37%, depending on your tax bracket.

- Long-term gains: If you profited from selling crypto you held for more than one year, it would be taxed as a long-term capital gain. Those capital gains tax rates are 0%, 15%, or 20%, depending on your taxable income that year.

Your gain depends on your cost basis. Your basis is typically the amount you originally paid for the crypto, plus any associated fees. However, if you happen to lose money on your crypto investment, you can use it to offset your gains and income. There is a $3,000 annual limit, but you can carry the remaining amount over to subsequent years when you file. To read more about this, check out How Crypto Losses Can Lower Your Tax Bill.

What tax forms report crypto transactions?

If you sold digital assets through a broker, you may receive Form 1099-DA, Digital Asset Proceeds from Broker Transactions. The IRS uses this form to report digital-asset proceeds from broker transactions. Generally, digital-asset sales are reported on Form 1099-DA rather than Form 1099-B. Keep any Forms 1099-DA and your transaction records to accurately report your gain or loss.

Save these tax forms, as they will help you accurately report your crypto gains and losses!

Note: As of 2026, for 2025 returns and later filing seasons, taxpayers may receive Form 1099-DA for certain brokered digital-asset transactions

FAQs about how to report cryptocurrency

Answers to more crypto FAQs

For more information on reporting virtual currency, the IRS has a helpful Frequently Asked Questions on Cryptocurrency Transactions page. This page gives detailed information on holding periods and different crypto activities and scenarios. You can also check out the official IRS webpage on virtual currency for more helpful publications.

The bottom line

Crypto taxes can feel complicated, but reporting them doesn’t have to be. If you sold digital assets, were paid in crypto, or earned crypto through mining or similar activity, make sure you report each transaction the right way and keep good records to support your return.

If you’re confused about the reporting requirements for cryptocurrency, our tax software can help. When you e-file with TaxAct®, we ask you questions about your crypto sales and guide you through the filing process step by step to ensure everything is reported correctly.

File your crypto taxes with TaxAct®.

This article is for informational purposes only and not legal or financial advice.

All TaxAct offers, products and services are subject to applicable terms and conditions.

All trademarks not owned by TaxAct, LLC that appear on this website are the property of their respective owners, who are not affiliated with, connected to, sponsored by, or sponsors of TaxAct, LLC.