Need help deciding between college savings plans with a tax-saving edge?

Here are the tax benefits for three basic plans specifically designed for college savings:

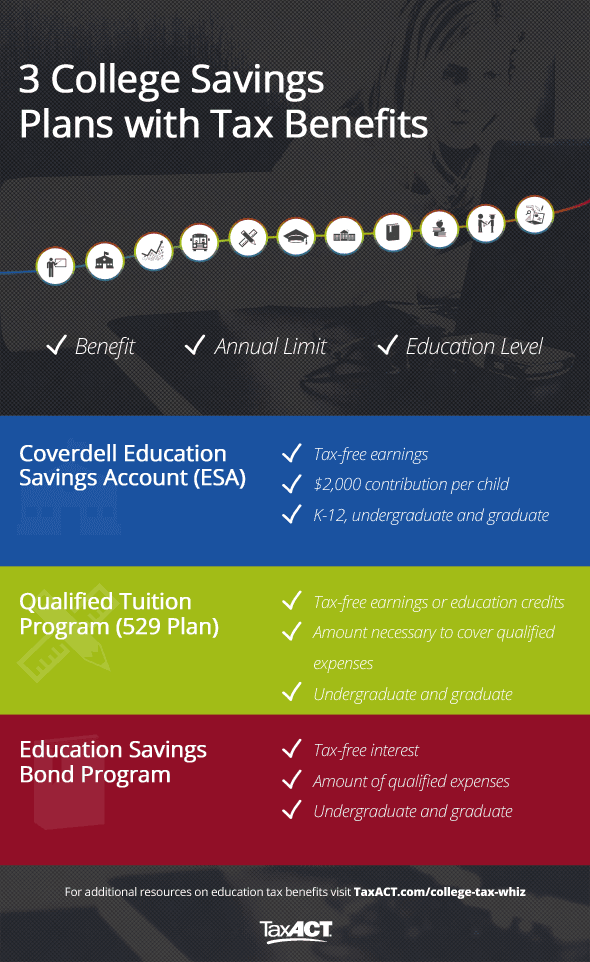

1. Qualified Tuition Program (529 Plan)

You’ve no doubt heard of Qualified Tuition Programs, commonly known as 529 plans. It’s a popular way to save for college, and you can use it as a savings plan or a prepaid tuition plan.

You make nondeductible contributions to an account. When it’s time to pay for college, you take tax-free withdrawals to pay tuition and fees.

That means you never pay tax on the interest and other earnings in the account if you use the withdrawals for qualified educational expenses. If you use the prepaid plan, you use tax-free education credits.

Advantages of a Qualified Tuition Program (529 Plan) includes:

- The account is in your own name, not the child’s. You still have control of the account. You don’t have to decide which child it is for, and you can even reclaim the amount you contributed in an emergency or for any other reason.

- The contribution limits, which are determined by state, can be significantly higher than other programs.

- You don’t have to worry about whether you’ll make too much money to benefit from 529 plans when the time comes. These plans are not restricted based on income level.

2. Education Savings Bond Program

U.S. Savings Bonds are similar to Qualified Tuition Plans in that you purchase them in your name, not the child’s. It can be Series EE bonds issued after 1989, or Series I bonds.

You’ll want to buy these bonds when the child is young in order to give the bonds time to earn substantial interest.

The bonds earn interest tax free. When you need the bonds for college expenses, you cash in the bonds. You don’t pay tax on the bond interest to the extent the expenses meet the qualifications.

You may be disappointed, however, if your income when you want to use the bonds is higher than it was when you bought them.

This tax benefit starts to phase out at a modified adjusted gross income level of $72,850 ($109,250 if married filing jointly).

If you’ve changed your mind, you can switch money from U.S. Savings bonds to another college savings plan. You can cash them in and make contributions to Qualified Tuition Programs or Education Savings Accounts.

3. Coverdell Education Savings Account (ESA)

Unlike the other two plans, Coverdell Education Savings Accounts are made in the name of the student, not the parent or benefactor.

With an ESA, you make nondeductible contributions to a child’s plan, before the child reaches age 18 (or any age for a special-needs child).

Come college time, the child takes distributions to pay for tuition, fees, necessary supplies and equipment, and even room and board if the student attends at least half time.

The child doesn’t even need to wait for college if he or she needs money for K-12 studies.

Another unique feature of ESAs is that you can use distributions for elementary and secondary education, if desired.

There’s one major limitation to ESA plans.

You can only contribute $2,000 per year for each child.

If more than one person contributes, for example if grandma wants to help, the total amount everyone contributes on behalf of any one child cannot exceed $2,000.

You’ll have to start early if you want to save enough to cover a major portion of a child’s college costs.

You also may be out of luck for the tax break if you are in a high-income bracket when you need to use the money.

The benefit starts to phase out at a modified adjusted gross income level of $95,000 ($190,000 if married filing jointly).

Do you think teenagers should help save for their college educations?

TaxAct makes preparing and filing your taxes quick, easy and affordable so you get your maximum refund. It’s the best deal in tax. Start free now or sign into your TaxAct Account.

Photo Credit: ileohidalgo