Updated for tax year 2025.

As the baby boomer generation ages, more taxpayers are handling estate and trust taxes for the first time. According to Accounting Today, the number of income tax returns for estates and trusts (Form 1041) increased by 14.9% between 2020 and 2021. But for many of us, handling taxes for an estate or trust can feel like deciphering a foreign language.

This guide will walk you through the essentials, breaking down Form 1041 filing requirements, instructions, and tips to make your tax preparation less daunting.

At a glance:

- Income generated between the owner’s death and asset transfer to beneficiaries must be reported to the Internal Revenue Service on Form 1041.

- Beneficiaries are responsible for paying income tax if assets are distributed before earning income.

- Not all trusts and estates must file Form 1041 — only those with income-producing assets or nonresident alien beneficiaries.

- The due date for Form 1041 depends on the tax year, which can be the calendar year or a fiscal year chosen by the executor.

What is IRS Form 1041?

IRS Form 1041 is the U.S. Income Tax Return for Estates and Trusts. It is used to report income earned by a decedent’s estate or trust after the estate owner’s date of death but before assets are distributed to beneficiaries. Just don’t confuse Form 1041 with Form 706, the United States Estate (and Generation-Skipping Transfer) Tax Return. Form 706 is a one-time estate tax return that reports the total asset value at death to calculate the potential estate tax.

When a person passes away, their estate becomes a separate taxable entity. Any income this entity earns — from rental income, capital gains, interest, or dividends — must be reported on IRS Form 1041. Similarly, income earned by certain trusts is also reported on this form.

Different schedules, such as Schedule D (capital gains and losses) and Schedule K-1, are also attached to Form 1041 to report specific types of income or the beneficiary’s share of income.

How does Form 1041 differ from Form 1040?

Form 1040 is used to report the income of an individual taxpayer, while Form 1041 is used for the decedent’s estate or a trust. For example:

- Form 1040 covers the income earned by an individual before their date of death.

- Form 1041 handles income earned by the estate or trust after the individual’s death.

For example, if someone dies before receiving their final paycheck, the money from that paycheck will be transferred to their estate. If the estate receives unpaid compensation, it may need to be reported on Form 1041. But someone must also file a final return (Form 1040) for the deceased — usually a spouse, another close relative, or an attorney. This will report all their income earned in the final tax year while they were alive.

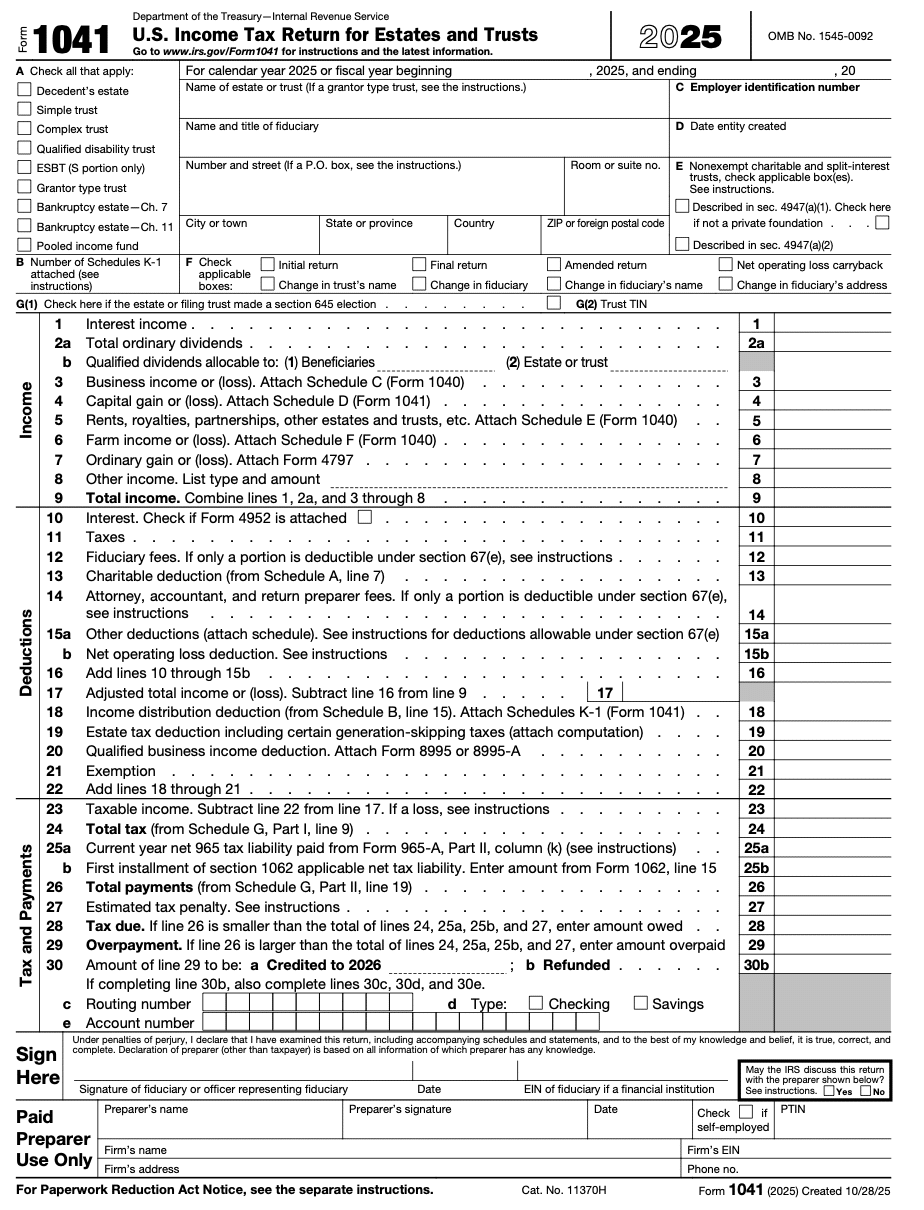

Form 1041 example

Here’s what the first page of IRS Form 1041 looks like:

Make sure to gather all the financial documents necessary to support the tax deductions you want to claim on Form 1041. For help with this, check out our Form 1041 tax preparation checklist.

Form 1041 instructions: Who needs to file Form 1041?

When filling out the three-page form, you’ll need to report the following information:

- General information. At the very start of the form, you’ll fill out basic information, such as the name of the estate or trust, address, EIN, name and title of the fiduciary, date, etc.

- Income. This is where you’ll report the amounts for the different types of income you may have earned. When finished, you’ll add them together and enter a total.

- Deductions. This section allows you to report any eligible deductions you’d like to claim.

- Tax and Payments. Here you’ll figure your taxable income, total tax, total payments, tax due, overpayments, and any other related information.

- Schedule A. This section is meant for a charitable deduction. You shouldn’t complete this section if you’re filing Form 1041 for a simple trust or pooled income fund.

- Schedule B. You’ll fill out this section if you’re claiming an income distribution deduction.

- Schedule G (Part I). This portion of Schedule G is for tax computations. Here you can figure tax and credit totals.

- Schedule G (Part II). The second part of Schedule G is for payments. This includes payments from other forms, federal income tax withheld, total payments, and more.

- Other Information. This section is dedicated to any other information that hasn’t been covered on the form. Much of this section asks whether the estate or trust received certain payments, earnings, distributions, etc.

Who needs to file Form 1041?

The fiduciary (executor, administrator, or trustee) managing the estate or trust is responsible for filing Form 1041 to report any income tax liability of the estate or trust.

You must file Form 1041 if the estate or trust meets any of the following criteria.

The fiduciary (executor, administrator, or trustee) managing the estate or trust is responsible for filing Form 1041 to report any income tax liability of the estate or trust.

You must file Form 1041 if the estate or trust meets any of the following criteria.

Decedent’s estate

The fiduciary (or one of the joint fiduciaries) must file Form 1041 for a domestic estate that has:

- Gross income for the tax year of $600 or more, or

- A beneficiary who is a nonresident alien.

- If you held a qualified investment in a qualified opportunity fund (QOF) at any time during the year, you must file your return with Form 8997 attached.

If the estate generates no taxable income and has no nonresident alien beneficiaries, there’s no need to file Form 1041.

An estate is a domestic estate if it isn’t a foreign estate. A foreign estate earns income from sources outside the United States. This income is not connected to any trade or business in the U.S. and is not part of gross income. If you are the fiduciary of a foreign estate, file Form 1040-NR, U.S. Nonresident Alien Income Tax Return, instead of Form 1041.

Trust

The fiduciary (or one of the joint fiduciaries) must file Form 1041 for a domestic trust taxable under section 641 of the Internal Revenue Code that has:

- Any taxable income for the tax year,

- Gross income of $600 or more (regardless of taxable income), or

- A beneficiary who is a nonresident alien.

- If you held a qualified investment in a qualified opportunity fund (QOF) at any time during the year, you must file your return with Form 8997 attached.

A trust is a domestic trust if it meets both of the following tests:

- Court test: A U.S. court can exercise primary supervision over the trust administration.

- Control test: One or more U.S. persons have the authority to control all substantial decisions of the trust.

A trust that isn’t a domestic trust gets treated as a foreign trust. If you are the trustee of a foreign trust, you must file Form 1040-NR instead of Form 1041. Also, a foreign trust with a U.S. owner generally must file Form 3520-A, Annual Information Return of Foreign Trust With a U.S. Owner.

Exceptions

If the trust (or a portion of the trust) is a grantor type trust, it must follow special reporting requirements outlined by the IRS in Instructions for Form 1041 and Schedules A, B, G, J, and K-1, page 13. Grantor trusts allow the grantor (the person or people who created the trust) to have certain powers and ownership benefits. Grantor trusts are generally ignored for income tax purposes, and the IRS considers the income, deductions, etc., as belonging to the grantor.

Note: Two or more trusts are treated as one trust if the main reason for the trusts is to avoid paying taxes AND they have the same grantors and beneficiaries. This rule only applies to the portion of the trust that comes from contributions (assets added to the trust) after March 1, 1984. In other words, any money or property added to the trust after that date will be subject to this “combining” rule if the criteria are met.

Common mistakes when filing Form 1041

Tax forms can be confusing, and it’s easy to make mistakes when filing. These are a few common mistakes people make when filing Form 1041 and how to avoid them:

Missing the Form 1041 deadline

Missing deadlines can lead to penalties, so keep track of when the estate or trust’s tax year ends. Form 1041 is due on the 15th day of the fourth month after the tax year ends. Be sure to keep track of deadlines and remember that due dates may change if the 15th falls on a weekend or holiday.

Incorrect information on Form 1041

Another common mistake is incorrectly reporting information on Form 1041. Reporting incorrect information, like misclassifying income on the form, can lead to penalties and underreporting. Be sure to have beneficiary information and income statements on hand.

Inaccurate filing or failing to distribute Schedule K-1s (Form 1041)

Similar to incorrect information on Form 1041, it’s important that you accurately file all information on each Schedule K-1 (Form 1041), and that you distribute the forms to each beneficiary. Keep in mind that the deadline for Schedule K-1 (Form 1041) is the same as the deadline for Form 1041.

Income to report on Form 1041

Income for Form 1041 includes money earned by the estate or trust from sources such as:

- Rental income

- Capital gains from investments

- Dividends and interest

- Income tax liability for the estate or trust

- Business income

- Final paychecks

It’s essential to separate income earned before and after the date of death, as only the latter is reported on Form 1041. The former gets reported on Form 1040.

Common deductions for estates and trusts

Here is a short list of common tax deductions and exemptions that can lower the estate’s taxable income:

- $600 exemption

- Executor fees (deductible if the estate pays the executor for their services)

- Professional fees for lawyer and accountant costs

- Administrative expenses, such as court filing fees

- Required distributions to beneficiaries

- Charitable contributions made by the estate or trust

When claiming deductions or tax credits, note that you may also have to file Schedule I, which is used to figure alternative minimum tax for estates and trusts.

How to calculate the income distribution deduction for Form 1041

The income distribution deduction allows an estate or trust to reduce its taxable income by the amount of income it distributes to its beneficiaries during the tax year. This deduction ensures that income is taxed only once — at the beneficiary’s level — rather than both the trust and beneficiary being taxed on the same income.

To calculate this deduction, use the distributable net income (DNI) as the maximum limit. DNI represents the estate or trust’s total income minus certain allowable deductions like charitable deductions and expenses for administering the estate. Distributions to beneficiaries cannot exceed the DNI amount. To avoid errors on Form 1041 and Schedule K-1, make sure you properly assign income and document how it was distributed.

Fiduciary income tax brackets

For tax year 2025, trusts and estates are taxed at the following rates:

| Income | Tax rate |

|---|---|

| $0 to $3,150 | 10% |

| $3,150 to $11,450 | 24% |

| $11,450 to $15,650 | 35% |

| Over $15,650 | 37% |

Form 1041 FAQs

Reporting income from estates and trusts: How to file Form 1041 with TaxAct

Filing Form 1041 doesn’t have to be complicated! TaxAct’s intuitive tax software guides you through the process step by step, ensuring you meet all the filing requirements while helping you maximize any tax deductions or credits available to the estate or trust.

Head over to TaxAct Estates and Trusts to get started. If you need help during the tax filing process, we also have detailed instructions for:

- How to enter distributions from Form 1041

- How to enter deductions for Form 1041

- How to enter Schedule K-1 for Form 1041

Need more time to file Form 1041? Don’t forget that TaxAct can also help you file an extension for Form 1041 by submitting Form 7004 to the IRS. Dealing with estate and trust taxes is taxing enough — this ensures you can take the necessary time to prepare while avoiding penalties for late filing.

The bottom line

Filing taxes for an estate or trust may not be your idea of fun. But with TaxAct’s help, filing Form 1041 doesn’t have to feel impossible. By understanding Form 1041 and staying organized, you’ll conquer your income tax return like a pro this year.

All TaxAct offers, products and services are subject to applicable terms and conditions.

This article is for informational purposes only and not legal or financial advice.