Updated for tax year 2025.

Are you ready for a new set of wheels? A new vehicle is a significant expense that requires careful consideration for most families. If you’re on the fence about which car-buying method is right for you, keep reading to discover the pros and cons of buying versus leasing.

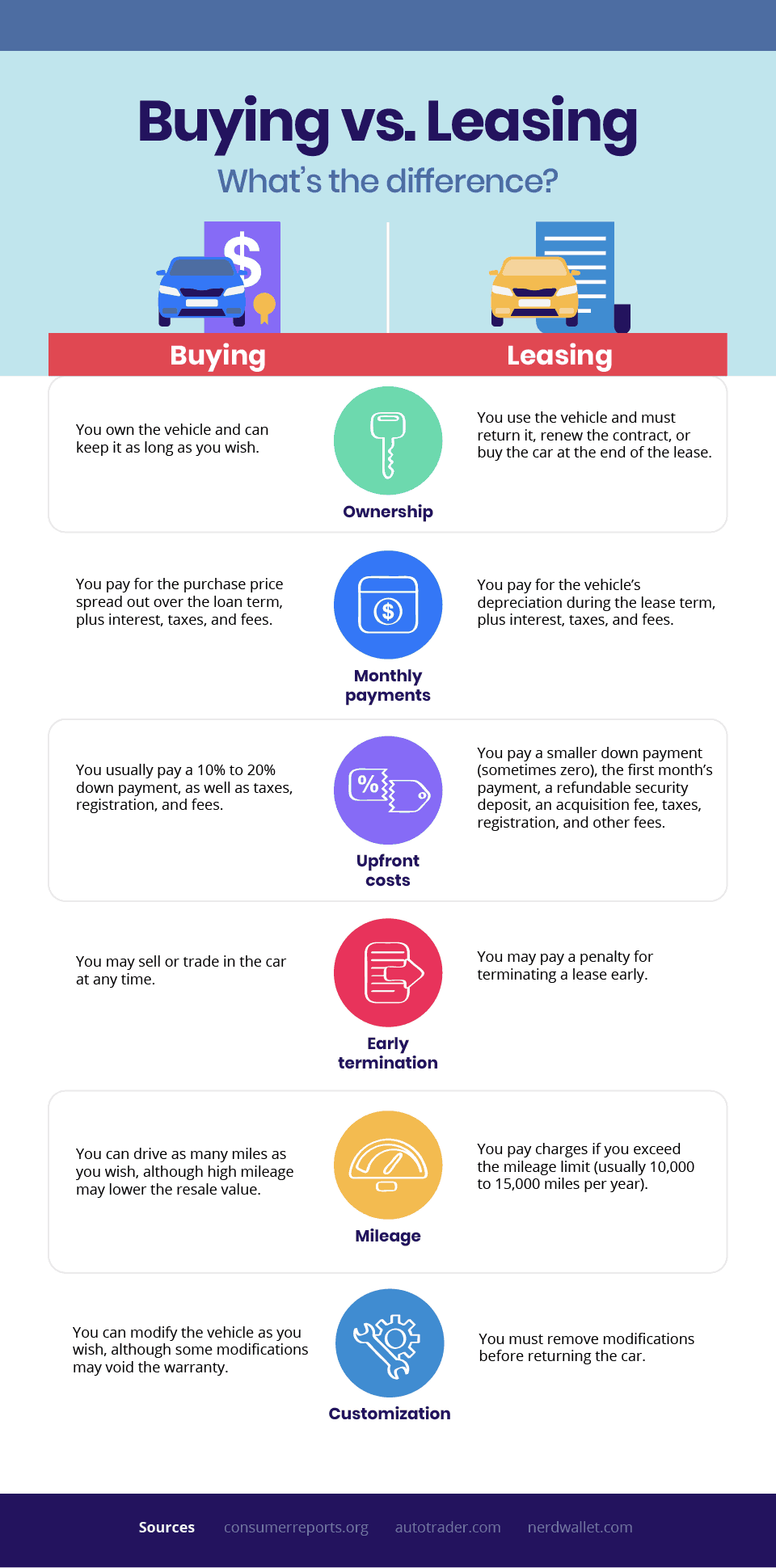

When it’s better to buy

A car lease usually requires less upfront costs and monthly payments than buying, but purchasing a vehicle is generally cheaper in the long run. Each option has benefits depending on your situation, but buying is probably the better option if any of the following are true for you:

1. You don’t mind a slightly used car.

Usually, purchasing a used vehicle is the most financially savvy decision. That’s because you avoid steep first-year depreciation. The actual depreciation rate depends on many factors, but many new cars lose 20% of their value in the first year and are worth much less than their purchase price after the first five years.

Another perk of buying used is that insurance and vehicle registration fees are usually lower for slightly used cars. However, keep in mind that repair and maintenance costs may be higher. And if you can buy a used car with cash, you’ll skip interest on loan payments and come out even further ahead financially.

2. You plan to keep your car for a long time.

Many Americans tend to keep their cars for several years. If you plan on driving your car for eight years or more, buying is usually the better option, especially if you can pay off the car loan and build equity.

3. You drive a lot.

One of the cons of leasing is that most leasing companies impose mileage restrictions and typically charge 15 to 25 cents per mile for each mile driven over a set limit (usually 10,000 to 15,000 miles per year). That excess mileage can add up quickly. You can negotiate a higher mileage limit, but you’ll likely have to pay more for the lease.

When you purchase a vehicle, you don’t need to worry about mileage limits; however, keep in mind that vehicles with high mileage often have a lower resale and trade-in value.

4. You’re hard on cars.

Buying is usually the way to go if you have young kids or haul heavy machinery in your car. When you return a leased car, a little wear and tear is okay, but generally, the vehicle needs to be close to its original condition. If it shows excessive wear, you’ll likely be charged for damages. You may also need to provide documentation showing that you have had all recommended oil changes, tire rotations, and tune-ups.

5. Your credit isn’t perfect.

Securing an auto loan is often easier than getting a good lease deal, especially if you’re rebuilding your credit. Auto loans typically have more lenient qualification criteria than leases, which are stricter and less accommodating of past credit issues. Leasing contracts can often have tighter credit requirements than auto loans, making them a less accessible option if your credit score isn’t in great shape.

6. You’re financing a new vehicle that qualifies for the car loan interest deduction

For tax years 2025 through 2028, the One Big Beautiful Bill Act lets qualifying buyers deduct up to $10,000 per year of interest on a loan for a new, U.S.-assembled passenger vehicle, even if you take the standard deduction.

Leases don’t qualify; only interest on a purchase loan counts. Here’s how it works:

- The vehicle must be new to you (not used)

- The loan must be secured and taken out after Dec. 31, 2024

- The deduction phases out above $100,000 MAGI (single) or $200,000 (married filing jointly).

Note: If you’re mainly using the car for business, different business vehicle rules apply instead.

When it’s better to lease

While there are many pros to buying a car outright, it isn’t always the better option. If any of the following are true for you, you may want to lease your next vehicle.

1. You’re self-employed and drive your car for business.

If you’re self-employed and drive for work, you may be able to deduct your lease payment. In this case, the deductible amount depends only on how often you use your car for business. For example, if your lease payment is $300 a month and you drive your car for business 50% of the time, you can deduct $150 a month as a business expense.

There’s one catch, though. You must subtract an “income inclusion” amount from your deduction if the car exceeds a certain value. This is an additional amount of income you may have to report if you lease a vehicle or other property for business purposes.

You must report the inclusion amount if the asset’s fair market value exceeds a certain threshold. The inclusion amount depends on how long you’ve leased your car and is calculated by looking up the amount on the IRS price table.

2. You always want the latest car with the newest technology.

If you want to upgrade your ride often, a leased vehicle may be a good option. Financing the entire purchase of a car you keep for less than three years usually doesn’t make financial sense. However, if a car is expected to have a higher-than-average resale value, it may still be worth buying.

3. You want cheaper upfront costs and lower monthly payments.

When you lease, you only pay for the difference between the sticker price and the car’s expected value at the end of the lease, plus interest rates and fees. You may not even need a down payment if you have excellent credit. It’s almost always cheaper in the short term to lease a car rather than buy it.

While leasing a new vehicle typically costs less out-of-pocket over a certain number of years, keep in mind that at the end of a leasing period, you don’t own the car and can’t resell it. That’s why purchasing a car is usually less expensive in the long term.

4. You want an electric car

Federal EV tax credits generally ended for vehicles acquired after Sept. 30, 2025, under the One Big Beautiful Bill Act. If you bought or took delivery on or before that date, you may still claim the credit when you file.

The old lease loophole, where dealers passed along commercial credit on leased EVs, is largely gone for new deals. Don’t assume you’ll get $7,500 off your payment; get any discount in writing on an itemized deal sheet.

Despite these changes, leasing can still make sense if you want lower upfront costs, plan to upgrade often, or want to avoid fast EV depreciation and mileage caps.

The bottom line

Before you get behind the wheel of your next new car, it pays to research the pros and cons of buying vs. leasing. Learn about the tax advantages and run cost comparisons before you make a decision, and whether you choose to buy or lease, don’t forget to enjoy the ride.

This article is for informational purposes only and not legal or financial advice.

All TaxAct offers, products and services are subject to applicable terms and conditions.

The OBBB is now also being referred to by lawmakers as the Working Families Tax Cut Act. You may see one or both names used here, but they refer to the same set of tax changes.