Affordable Care Act Tax Law Changes for Higher Income Taxpayers

File your taxes with confidence.

Your max tax refund is guaranteed.

Most taxpayers don’t need to worry about the new additional 3.8% tax on net investment income, or the additional 0.9% Medicare tax.

These taxes only apply to individuals (and estates and trusts) that have income over certain levels.

You generally won’t pay either of these taxes unless you make over $200,000 in one year.

If you are married and you file a separate return, you may pay additional taxes after your income exceeds $125,000.

You never pay both of these taxes on the same income.

The net investment income tax is based on investment income, such as interest and dividends, while the additional Medicare tax is levied on wages and other earned income.

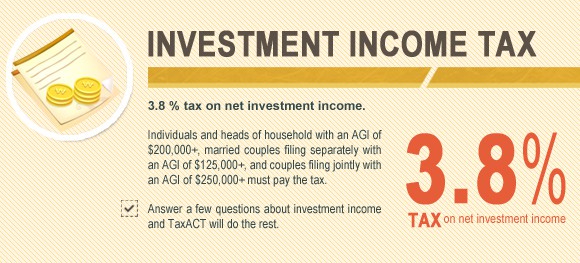

Net Investment Income Tax (NIIT)

Starting with your 2013 tax return, due when you file in 2014, you must pay an additional 3.8% on any “net investment income” if your modified adjusted gross income is more than $200,000 ($250,000 if married filing jointly, or $125,000 if married filing separately).

Investment income is generally money you receive when your money or other investments are working for you. This includes interest, dividends, capital gains, rental and royalty income, and non-qualified annuities.

Investment income does not include gain from the sale of your home that you can exclude. However, if you have gain from the sale of your home that you cannot exclude, you may owe net investment income tax on that amount.

Investment income does not include wages, unemployment compensation, Social Security benefits, alimony, tax-exempt interest, or self-employment income.

Before you pay the additional tax on investment income, you can deduct certain expenses. This includes allocable investment interest expense, investment advisory and brokerage fees, expenses related to rental and royalty income, and state and local income taxes allocable to the investment income.

TaxAct calculates the net investment income tax for you on Form 1040, if the tax applies.

Will I have to pay net investment income tax on my children’s interest, dividends, and capital gains that I report on my Form 1040?

You won’t pay this tax on your children’s income that you exclude from taxable income because of the threshold amounts on Form 8814, or amounts attributable to Alaska Permanent Fund Dividends.

However, you may pay the net investment income tax on the remaining portion of your children’s investment income if you report it on your return.

Because of this, if you are subject to the net investment income tax, you may want to file separate returns for your children.

Do I have to include the net investment income tax in my estimated tax payments?

Yes. You should take the new tax into account when you make your quarterly estimated tax payments, or you may owe additional taxes, penalty and interest.

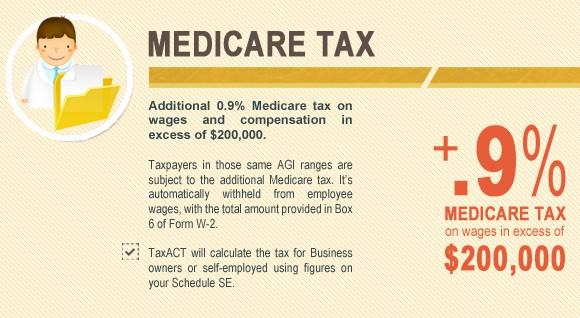

Additional Medicare tax

Another new tax for 2013 is the additional Medicare tax. You must pay this tax if your wages, compensation, and self-employment income, along with that of your spouse if filing jointly, is more than $200,000 ($250,000 if filing jointly, or $125,000 if married filing separately).

If you earn wages and you make more than $200,000 from one employer, your employer automatically withholds the additional amount from your paycheck.

The tax is 0.9% of your wages over $200,000.

The additional Medicare tax is different from regular Medicare tax in one regard. Unlike regular Medicare tax, the additional tax is not calculated on your earned income alone. It also takes your spouse’s income into consideration.

When TaxAct calculates the actual amount of additional Medicare tax you owe, it may be different from the amount you have withheld.

If you earn more than $200,000 in wages and compensation but are paid by more than one employer, neither employer withholds the additional tax. You pay the additional Medicare tax along with your other tax liability.

On the other hand, if you are married and you earn more than $200,000, but less than $250,000, and your spouse has no earned income, you may have Additional Medicare Tax withheld.

However, if you file jointly, you do not owe the tax because your total wages and compensation are not more than $250,000. Your total tax liability will be reduced by the amount of additional Medicare tax you have withheld.

How much does your tax rate on varying types of investments affect your investing decisions?

Photo credit: WanderingtheWorld (www.LostManProject.com) via photopin cc

More to explore:

File your taxes with confidence.

Your max tax refund is guaranteed.