10 Events to Consider When Planning Your Child’s Financial Future

File your taxes with confidence.

Your max tax refund is guaranteed.

You want the best for your children: good health, a great education and solid financial security.

And if you want that last part to include money for college or a financial lifeline for an accident or illness, the time to start planning is now — even if “now” means “while you’re still working on becoming a parent”.

Here are 10 important events to consider when planning your child’s financial future.

Growing Up with Special Needs

In addition to changes in day-to-day care and routines, raising a child with special needs can involve particular financial considerations.

This is especially true if your child’s needs require ongoing care or treatment.

Insurance, government assistance and other programs can often help pay for physical therapies, medical treatments or supplemental education, but it still helps to start saving early.

If your child will need additional care into adulthood, you may need to arrange your finances so he or she can still qualify for Medicaid and Supplemental Social Security.

To do this, you’ll need to keep money out of your child’s name. A trust can be a good option.

Going to School

Even if you plan to send your child to public school, you’ll need to save for school supplies, extracurricular activities like sports and music lessons, and summer enrichment camps.

And if you’re considering private school, the average tuition already tops $9,000 a year and is guaranteed to increase.

Getting an Allowance

Experts agree that giving your children some kind of allowance is a great way to teach financial responsibility.

A debate remains over how to distribute the money, though.

Should it be tied to chores or school performance? Divided into saving, spending, and giving? And what age is old enough?

Regardless of what you decide, you’ll need to budget for extra pocket money each month.

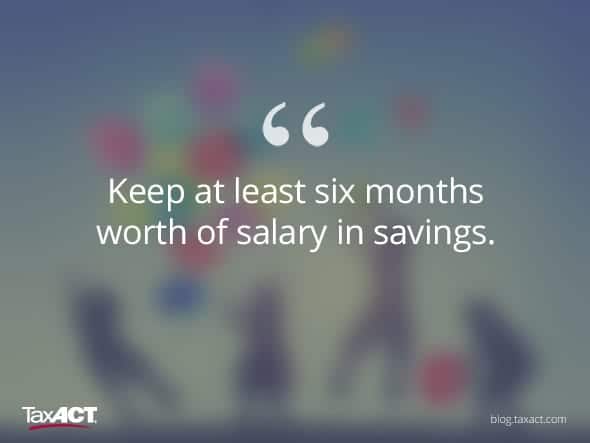

Recovering After an Accident

If you were injured in an accident and unable to work, how would you provide for your family?

The best protection is to invest in disability insurance, either through an employer or privately.

Another smart idea is to keep at least six months’ salary in savings.

Recovering from a Parent’s Death

While we’re on grim subjects: What if you or your spouse died? It’s terrible to think about, but even worse not to plan for.

In most cases, both parents should have a life insurance policy equal to several years’ salary (or as much as you can afford to carry).

Do you have a last will and testament?

Not having one is often the biggest mistake most people make. More than half of all Americans die without one.

If you don’t have a will when you die, state law determines who gets your money and other assets and determines who your personal representative is.

If you have minor children, the court decides who will raise them.

Simply put, make it easy for those you love, plan now.

Have adequate life insurance coverage and a last will and testament in place.

Buying a Car

Not every 16-year-old needs a car, but not every parent has the time to personally drive teenagers to every practice, lesson and appointment.

If you foresee the need for a car, talk with your teen about ways to share the cost, including fuel and insurance.

Getting a Job

In many families, kids are expected to work outside the home to earn money for extras like clothes, movies and activities with friends.

If that’s your plan, start your kids thinking about jobs early.

As a general rule, younger children can babysit or walk dogs as early as 13, while older kids can work restaurant or lawn care jobs after school or during the summer.

Going to College

Tuition at both public and private colleges has skyrocketed over the past 30 years, and the trend is expected to continue.

Instead of pinning your hopes on a full-ride golf scholarship, start investing early in a 529 Plan or Coverdell Education Savings Account.

Both savings plans let you withdraw funds tax-free for qualifying education expenses.

Being Unemployed

Again, unemployment is a great reason to keep at least six months’ salary in an easily accessible savings account.

If you suspect that you might lose your job in the next year, try your best to live on only one salary.

If it’s your adult child who’s unemployed, set ground rules for moving back home, and if you have to lend money, attach real terms and interest.

Getting Married

Traditionally, the bride’s parents pay for the wedding — an average of $25,000 in 2014.

But it’s increasingly common for families, along with the couple themselves, to share the costs. If you are planning to help your child pay for a wedding, start saving now.

And if your child opts for a low-cost, DIY wedding, you may find other good uses for that money — like helping out with a down payment on a first home.

The bottom line, and theme woven throughout all of these scenarios, is to start saving and planning now.

More to explore:

File your taxes with confidence.

Your max tax refund is guaranteed.